Key Takeaways:

- Real-world assets (RWAs) utilise distributed ledger technology to track assets, with performance derived from sources outside the blockchain.

- There are two main ways of tokenising RWAs for native and non-native tokens.

- Currently, RWA protocols backed by money market funds, bonds, and equities dominate the market with ~60% market share in terms of total value locked (TVL), followed by RWA lending and real estate.

- The tokenisation of financial and real-world assets has the potential to become the game-changing use case that drives blockchain breakthroughs.

- Tokenisation is estimated to grow by a factor of 80 times in private markets and potentially reach a value of nearly US$4 trillion by the year 2030.

Introduction to RWAs

Real-world assets (RWAs) utilise distributed ledger technology (like blockchain) to track assets, with performance derived from sources outside the blockchain. They are tangible or intangible assets that can be tokenised and represented as digital tokens on the blockchain. And they are gaining traction: According to a report by Boston Consulting Group, the on-chain RWA market is projected to reach US$4 trillion to US$16 trillion by 2030.

RWA tokens are essentially representations of assets that are not inherently native to a blockchain, and they differ from volatile assets commonly associated with cryptocurrencies. They possess programmable capabilities, enabling the inclusion of features like lockup periods and requirements for accredited investors.

Examples of RWAs include the issuance of tokens that represent ownership in real estate investments or participation in funding initiatives for entrepreneurs in developing nations. Although these tokens exist on a blockchain, the underlying assets take place in the physical world.

How Real-World Assets Are Tokenised

There are two main ways of tokenising RWAs:

Non-native tokens

- On-chain tokens are issued to represent RWAs that are managed off-chain.

- The more common way (due to the early stage of RWAs), an advantage is leveraging existing financial infrastructure around asset custody.

- As an example: All existing USD-collateralised stablecoins are currently in the form of a non-native token.

Native tokens

- An on-chain token is issued and acts as the RWA itself. In other words, the token does not represent any other off-chain asset.

- For instance, the European Investment Bank issued €100 million two‑year digital bonds on the Ethereum public blockchain in 2021.

Advantages of Tokenisation

There are various advantages of RWA tokenisation:

Transparency: The true value of an asset can be reflected on-chain.

Efficiency: Distributions to asset owners can be facilitated through their crypto wallets.

Liquidity: The on-chain nature of blockchain enables the buying and selling of assets that were previously illiquid.

Self-custody: Individuals have the ability to retain control over their assets.

Collateralisation: Assets can potentially be utilised as collateral on decentralised finance (DeFi) protocols.

Are Real-World Assets Used Yet?

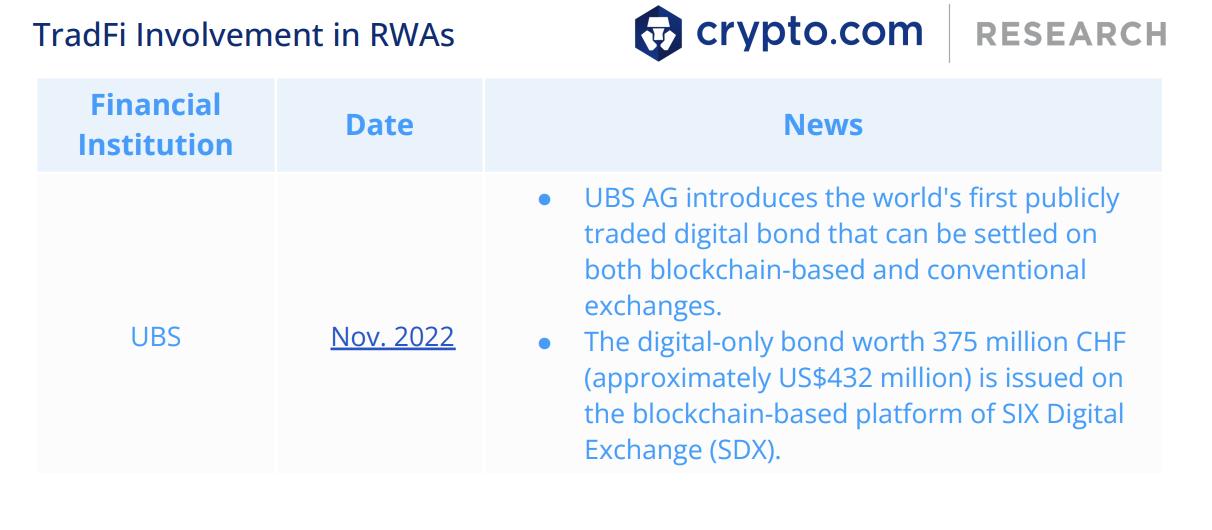

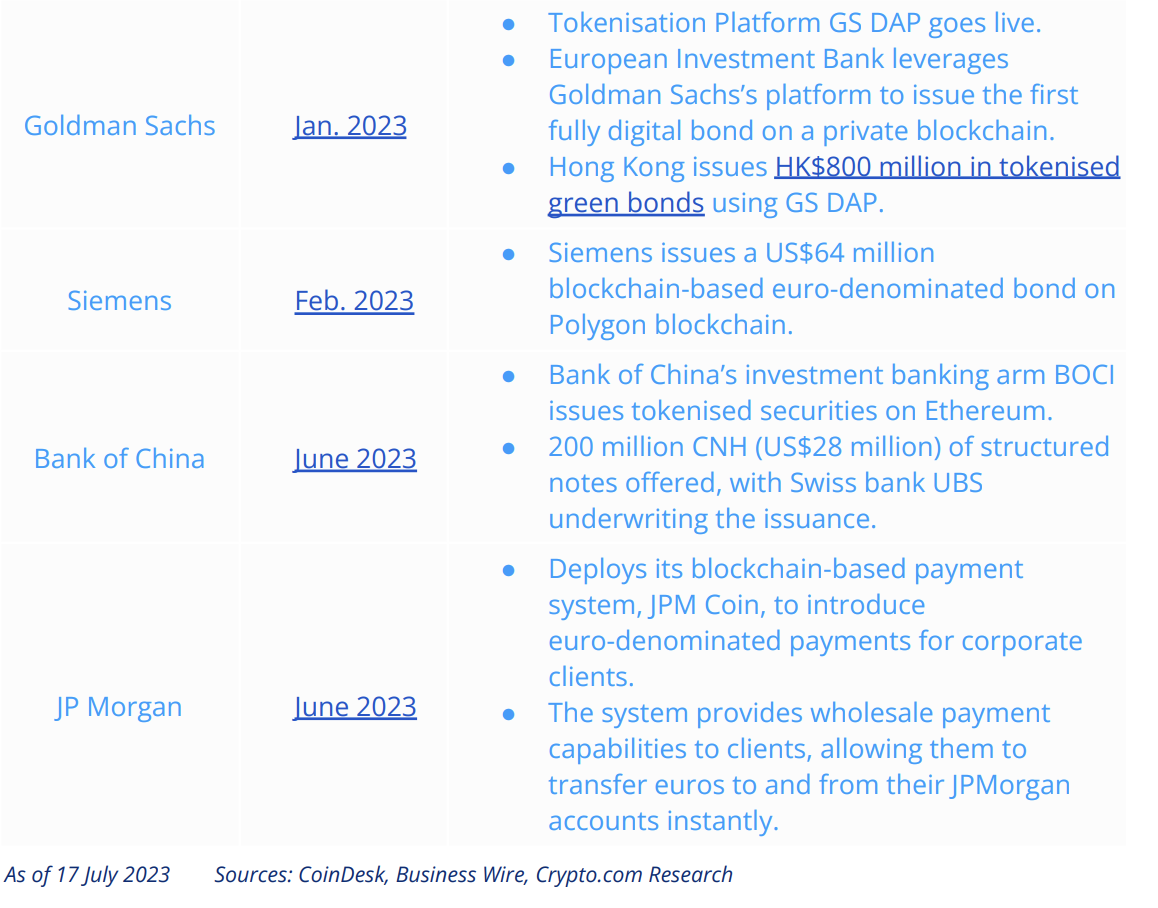

Yes. Traditional finance (TradFi) has started participating in tokenising real-world assets, as more and more financial giants are beginning to establish their presence in this field.

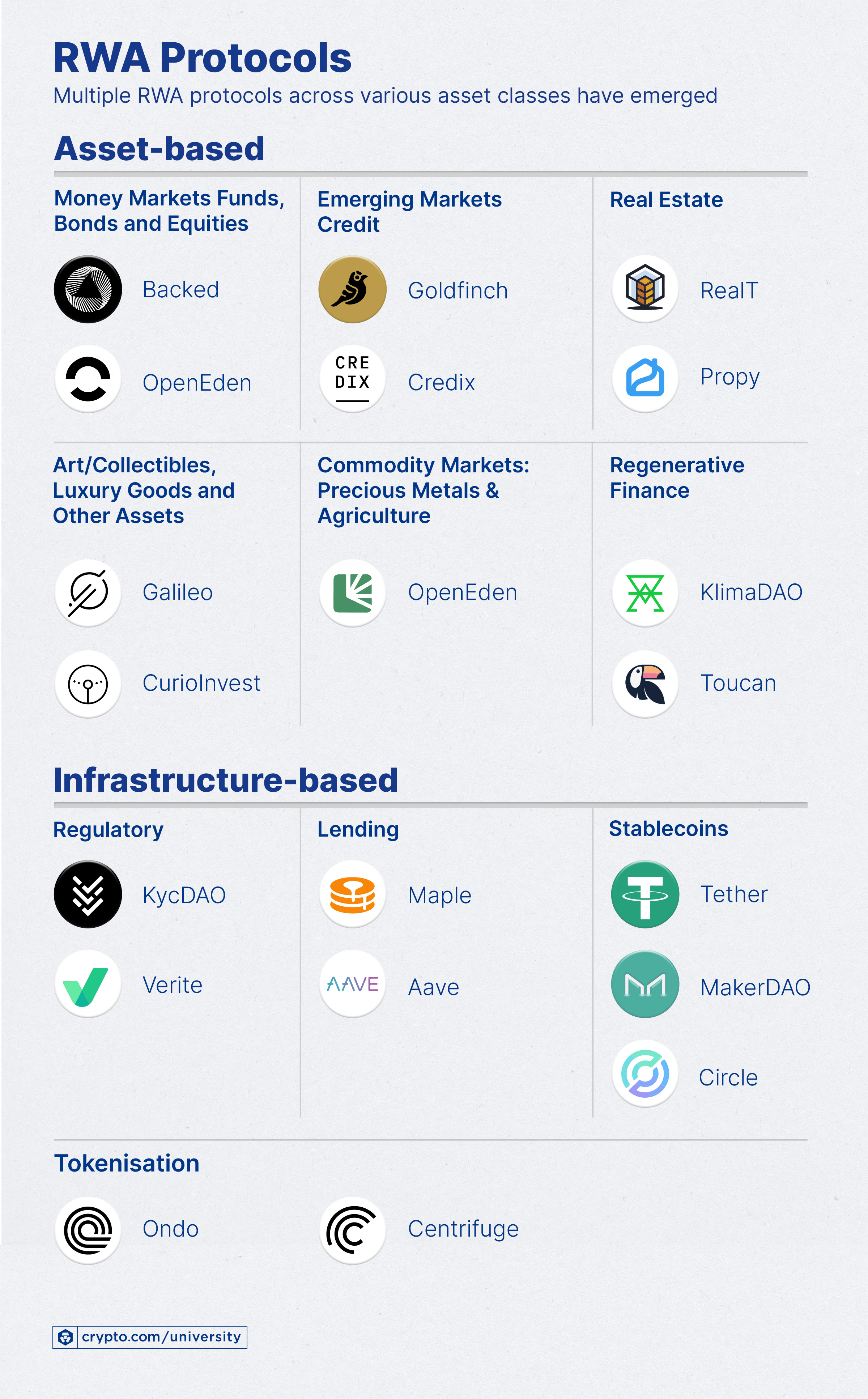

Who Is Creating RWAs in the Crypto Space?

There are various RWA protocols capable of tokenising RWAs from a wide variety of asset classes, including:

- Money markets (e.g., term certificates of deposit of interbank loans, money market mutual funds, commercial paper, Treasury bills)

- Equity and Debt markets (e.g., stocks and bonds)

- Real estate (e.g., property consisting of land and the buildings on it)

- Carbon markets (e.g., trading systems in which carbon credits are sold and bought)

- Luxury goods (e.g., designer handbags, high-end watches, jewellery)

- Commodity markets (e.g., gold, oil, coffee, soybeans)

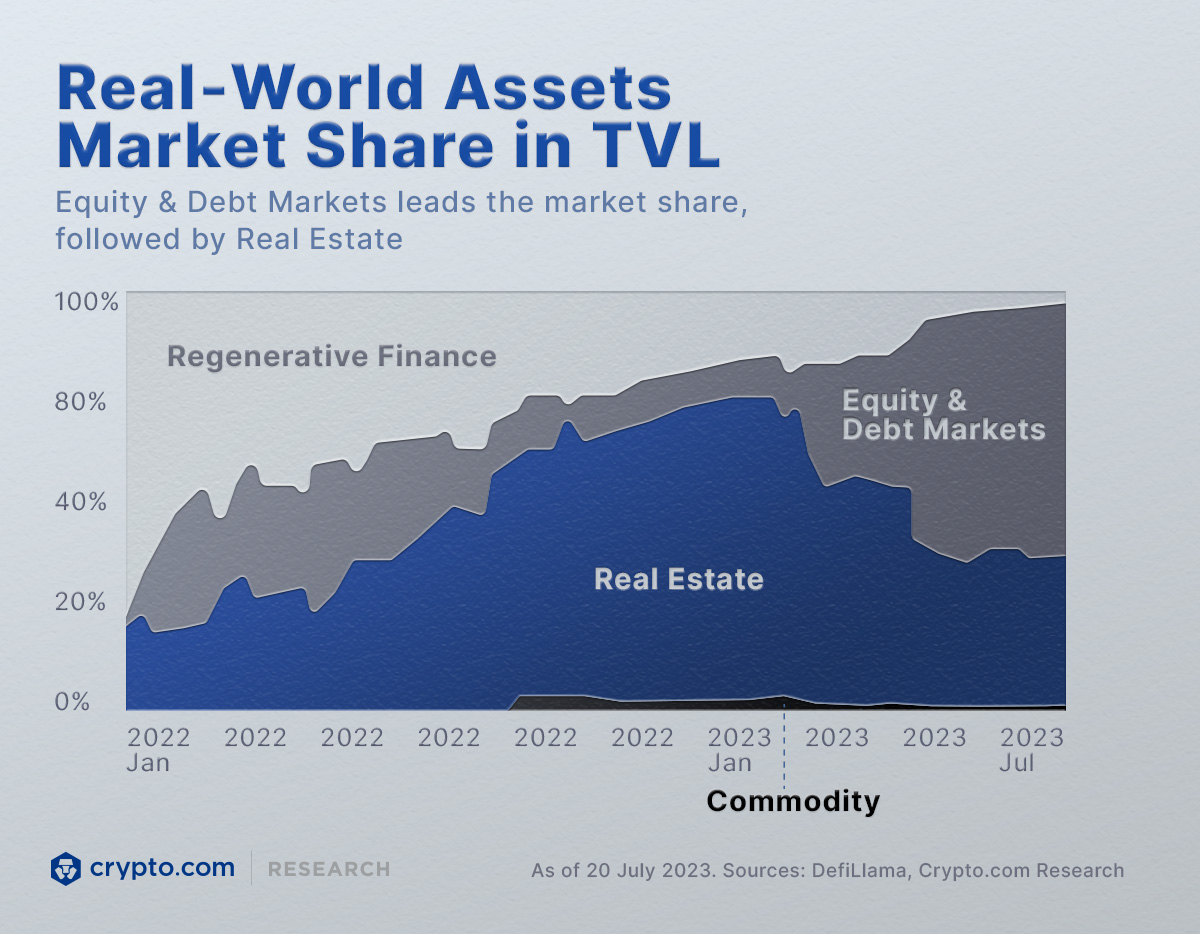

The below graphic shows an overview of RWA protocols by market:

Currently, the Equity & Debt Markets category has been dominating the RWA market share since Q2 2023, as seen in the data shown below. Additionally, RWA lending and real estate are other popular asset categories. Meanwhile, it is also notable that regenerative finance like the carbon market has significantly plummeted.

For a deep dive into some of the most popular RWA protocols, read the full Research report by our Research & Insights Team, which also includes sources for all facts and figures cited in this article.

Conclusion

Real-world assets (RWAs) are a transformative use case of blockchain technology, though they are still at the nascent stage and not quite at mass adoption yet. The potential of RWAs is limitless, however, as theoretically almost anything can be tokenised — from artwork, real estate, and carbon credits to financial instruments like bonds and stocks.

There are various challenges in the process of implementing RWAs, which include valuation and auditing, custody and security, governance, and trust, as well as interoperability and scalability concerns. Overcoming these obstacles requires significant collaboration amongst all stakeholders, including asset originators, token issuers, service providers, regulatory bodies, and traders.

Overall, the outlook for RWAs is promising. According to a Citi report, the tokenisation of financial and real-world assets has the potential to become the game-changing use case that drives blockchain breakthroughs. Citi suggests that tokenisation could grow by a factor of 80 times in private markets, potentially reaching a value of nearly US$4 trillion by the year 2030.

As blockchain technology continues to mature, and the landscape evolves, it is likely there will be increased adoption and integration of RWAs into the crypto space. While challenges persist, the potential benefits make RWAs an exciting frontier in the future crypto landscape.

Due Diligence and Do Your Own Research

All examples listed in this article are for informational purposes only. You should not construe any such information or other material as legal, tax, investment, financial, cybersecurity, or other advice. Nothing contained herein shall constitute a solicitation, recommendation, endorsement, or offer by Crypto.com to invest, buy, or sell any coins, tokens, or other crypto assets. Returns on the buying and selling of crypto assets may be subject to tax, including capital gains tax, in your jurisdiction. Any descriptions of Crypto.com products or features are merely for illustrative purposes and do not constitute an endorsement, invitation, or solicitation.

Past performance is not a guarantee or predictor of future performance. The value of crypto assets can increase or decrease, and you could lose all or a substantial amount of your purchase price. When assessing a crypto asset, it’s essential for you to do your research and due diligence to make the best possible judgement, as any purchases shall be your sole responsibility.